Intermediate

Macroeconomics

Lecture 7

Douglas Hanley, University of PittsburghCredit Market Imperfections

In This Lecture

- Credit market imperfections and consumption

- Asymmetric information and the financial crisis

- Limited commitment and the financial crisis

- Social Security Programs

Credit Market Imperfections

- Lenders (savers) face a lower interest rate than borrowers

- The government borrows and lends at the interest rate that lenders face

- This implies that Ricardian equivalence does not in general hold

- Government could essentially borrow on behalf of consumers

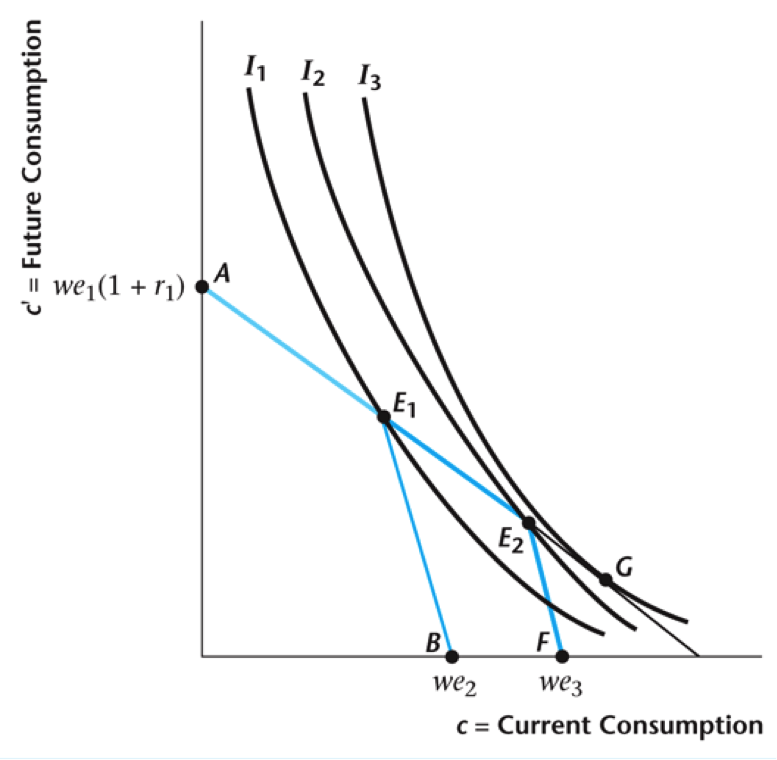

Different Interest Rates

We get a kink in the budget constraint at zero savings ($E$)

Effects of Credit Imperfections

- Now many consumers will neither save nor borrow

- This is call hand-to-mouth consumption

- About $1/3$ of American households live this way

- Most (about $2/3$) are not poor by traditional metrics: their assets are illiquid

- See “The Wealthy-Hand-to-Mouth” for more info

Effects of Delayed Taxation

Taxes reduced today and increased in the future ($E_1 \rightarrow E_2$)

Ricardian equivalence is broken here!

Effects of Delayed Taxation

- Here the consumer initially is credit constrained (zero savings)

- For such a consumer, today's tax reduction will go towards current consumption

- Very different from the case with no credit market imperfections, where the consumer will save the entire tax cut to pay higher future taxes

The Financial Crisis

- Two key credit market frictions: asymmetric information and limited commitment

- Asymmetric information: Would-be borrowers know more about their characteristics than do lenders

- Limited Commitment: Borrowers may choose to default (go bankrupt)

- lender can overcome limited commitment with collateral

Asymmetric Information

- Some default, some don't: bank can't tell difference

- Generally, saving/lending ($r_1$) and borrowing ($r_2$) interest rates are different

- Givn $a$ probability of repayment, banks balance sheet: $$\begin{array}{lc} \text{From Fed} & + 1 \\ \text{To me} & - 1 \\ \text{I repay?} & + a (1+r_2) \\ \text{To Fed} & - (1+r_1) \\ \hline \text{Profit} & a (1+r_2) - (1+r_1) \end{array}$$

Consumer Interest Rates

- If bank industry competitive (free entry), they should make zero profits $$1+r_2 = \frac{1+r_1}{a}$$

- As probability of repayment $a$ goes to zero, interest rate $r_2$ goes to $\infty$

- If people always repay ($a=1$), interest rates are same ($r_2=r_1$)

- Generally $a$ is lower for lower income consumers, so they face higher interest rates on borrowing

Decrease in Good Borrowers

Decrease in fraction of creditworthy borrowers shifts budget constraint inwards (banks trust them less)

Decrease in Good Borrowers

- Default premium increases — even good borrowers face higher loan rates

- Budget constraint shifts in, consumption falls for all borrowers

- Matches observations from the current financial crisis — increase in credit market uncertainty, reduction in lending, decrease in consumption expenditures

Market Uncertainty Over Time

Interest rate spread: interest rates on BAA-rated corporate debt (moderate risk) - AAA-rated corporate debt (low risk)

Limited Commitment and Credit

- If defaulting (not repaying) was costless, borrowers might often do so

- Banks create incentives for consumers not to default on debts

- Typically through collateral requirements — if you don't repay, bank takes your collateral

- Examples of collateral

- House is collateral for a mortgage loan

- Car is collateral for a car loan

Collateral Example

- Let $H$ be the quantity of housing owned by consumer (quality adjusted rooms, square feet, etc)

- There is a market price $p$ price of housing ($/quantity)

- Housing is illiquid — takes time and effort to sell

- Possible to borrow against housing wealth (use it as collateral)

Consumer's Constraints

- In the worst case, you have no money tomorrow but bank repossesses your house (and gets its value $pH$)

- This is the maximum you can pay back for sure next period $$\underbrace{-s(1+r)}_{\text{debt}} \le \underbrace{p H}_{\text{value of house}}$$

- This limits on how much we can borrow to consume today $$\begin{align*} & c + s = y - t \\ \Rightarrow &\ c \le y - t + \frac{pH}{1+r} \end{align*}$$

Budget Set With Collateral

Now there is a hard limit to current consumption

Collateral Constraint Effects

- The least you can optimally consume tomorrow is your net income $y^{\prime}-t^{\prime}$

- The most you can optimally consume is your income plus the value of your house $pH$

- As with asymmetric information, many will be exactly at the kink point (fully leveraged)

- Ricardian equivalence will still hold for unconstrainted consumers, but not for constrained ones

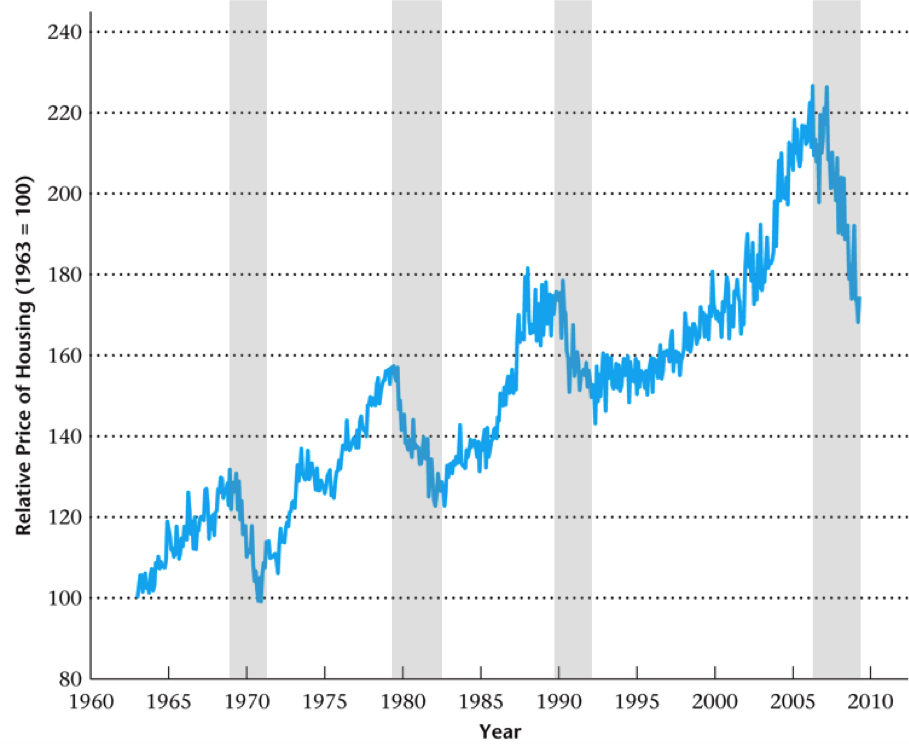

Relative Price of Housing

Large decline in US housing prices beginning in 2006

Deviations from Trend

Large decline in aggregate consumption in 2007

Recent Recession Price

Case-Shiller index of house prices since 2000

Social Security

- Government program that effectively saves on behalf of consumers

- Funded by Social Security tax levied approximately proportionally on workers

- Retired workers receive benefits starting at about age 65 (or a bit later)

Implementing Social Security

- Total revenues/outlays (roughly equal) are between 4 and 8% of GDP at a given time

- Two ways to implement: pay-as-you-go and fully-funded

- Both can work, but they share the cost differently between young and old people

Pay-as-you-go Social Security

- Taxes on current workers pay for social security of current retired

- For simplicity, suppose two generations alive at each date: young and old

- Young pay social security taxes $t$ and old receive social security benefits $b$

- Next period, the young become old, there is a new young generation, and the old die

Pay-as-you-go Budget Balance

- The population grows at constant rate $n$ so that $$N^{\prime} = (1+n) N$$

- Total benefits to old must equal total taxes on young $$N b = N^{\prime} t$$

- Combining these, the necessary tax rate for benefits $b$ is $$N b = (1+n) N \cdot t \quad \Rightarrow \quad t = \frac{b}{1+n}$$

Effect of Population Growth

- Remember we are thinking from generation to generation, so each period is 25 years

- In that case population growth is about $n = 30\%$

- At any given time taxes only have to be $1/(1+n) \approx 75\%$ of benefits

- Young generation is larger than old, so pays less per person to take care of old people

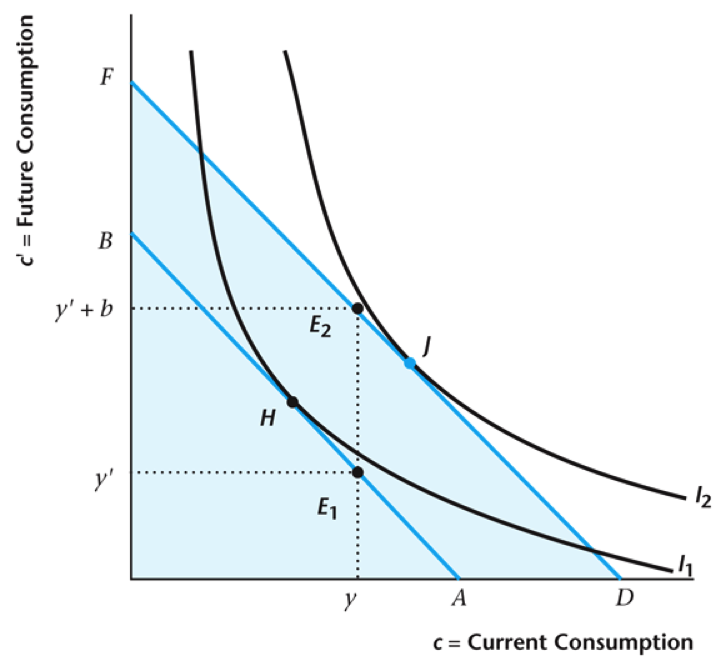

PayGo for Old Consumers

When the social security introduced:

old receive benefits $\rightarrow$ they're better off

PayGo for Young Consumers

If $n \ge r$, the budget constraint shifts out from AB to DF

$\rightarrow$ the consumer is better off

Pay-as-you-go Social Security

- Pay-as-you-go is beneficial only if the population growth rate exceeds the real interest rate.

- Change in wealth of young and later generations $$\Delta we = -t + \frac{b}{1+r} = -\frac{b}{1+n} + \frac{b}{1+r} = \frac{b(n-r)}{(1+n)(1+r)}$$

- If $n \ge r$, young have higher wealth and are hence better off

Intuition for Welfare Effects

- Is this a Ponzi/pyramid scheme? Technically yes, but it still works

- Suppose you have an infinitely long line of people $i = 0,1,2,\ldots$

- Each person but the first gives the person before them $\$10$ ($i \rightarrow i-1$)

- First person ($i=0$) is better off ($+\$10$) and everyone else is indifferent!

Fully-Funded Social Security

- Here consumers pay taxes while young and receive benefits of the same value (plus interest)

- Essentially a mandated savings program where assets are acquired by the young, with these assets sold in retirement.

- Money isn't just wasting away in the meantime, government invests this money in assets

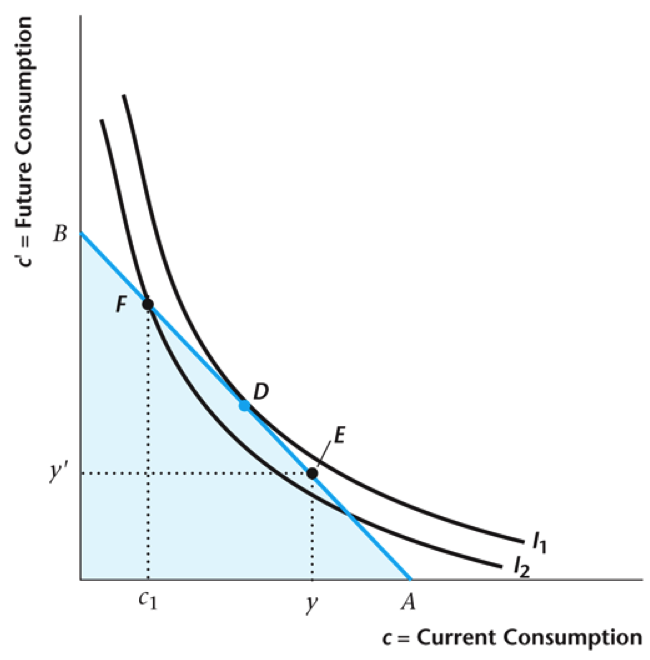

Fully Funded Social Security

With mandated saving amount, consumer must choose point F rather than D $\rightarrow$ is therefore worse off

Fully Funded Details

- The government mandates a certain miniumum level of savings, so there is only an effect when the consumer didn't want to save more than that already

- Can this be undone by Ricardian equivalence? (consumers borrowing to offset social security)

- Fully funded is often what people are referring to in proposals to privatize Social Security, as this savings could handled in personal accounts (and managed by banks)

Government Commitment Issues

- Might there be a rationale for choosing pay-as-you-go even if it doesn't look desirable? ($n \lt r$)

- Without Social Security, workers must save for their own retirement

- If someone doesn't save, can government commit to not helping them out when old?

- Similarly, people may invest in excessively risky assets, knowing they will be "bailed out" when older (moral hazard)

Positive and Normative

- We've been making a lot of normative statements about whether people are better off under various schemes

- Can also take a positive approach: given how certain groups are affected (young vs old, for instance), what policy would we expect to see?

Predicting Policy Outcomes

- We saw that the pay-as-you-go system is always good for old people, but only good for young people when the "return" to Social Security ($n$) is larger than the return on savings ($r$)

- Whether the system is implemented then becomes one of political economy: which groups are larger or have more political power?

Policy Transitions

- As population growth rates are falling ($n$ getting smaller), pay-as-you-go gets less desirable for some

- We might expect transitions from pay-as-you-go to fully funded systems

- This is being discussed seriously in some European countries

Transition to Fully Funded

- This transition leaves the current generation of old people out of luck

- They didn't know to save in preparation for this event (though many certainly did save)

- Taxing the young to fund the old would just be pay-as-you-go over again

- One solution is to have government borrow. Some countries have difficulty because of EU deficit limitations (3% in some cases)